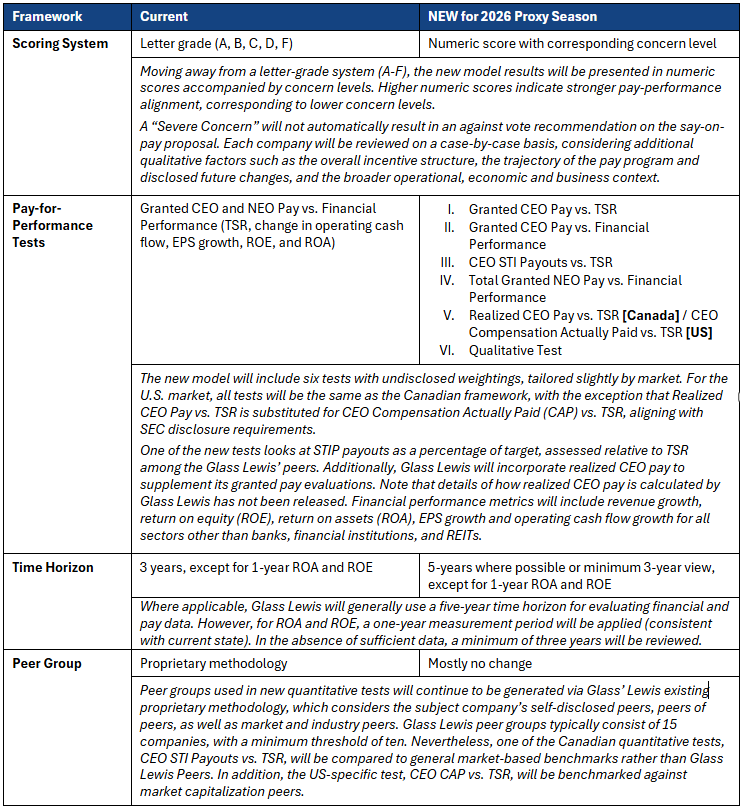

Effective in 2026, Glass Lewis will implement a new pay-for-performance model for U.S. and Canadian markets, replacing its current framework. The enhanced model aims to provide a more comprehensive review of executive pay and performance alignment. Key changes to the model are highlighted below:

Unlike ISS, which relies on reported grant date fair values for equity awards, Glass Lewis conducts its own valuation for equity-based awards. As a result, the granted CEO pay used in the Glass Lewis model often diverges from reported CEO pay in issuers’ proxy disclosure. In the new model, Glass Lewis is broadening its evaluation scope to incorporate CEO STI payout and realized pay. Another notable distinction is the construction of their proprietary peer groups. For Canadian-incorporated issuers, ISS limits its peer group to Canadian companies. In contrast, Glass Lewis peer groups typically include a broader set of North American peers, which enables the comparison of subject companies with US peers where relevant. This broader cross-border comparison may influence the underlying pay and performance alignment evaluation.

While Glass Lewis’ new model has experienced several significant changes, we expect that the model result and vote recommendations will not materially change. Southlea will continue to monitor and share updates released by Glass Lewis and the implications for companies as we approach the 2026 proxy season.